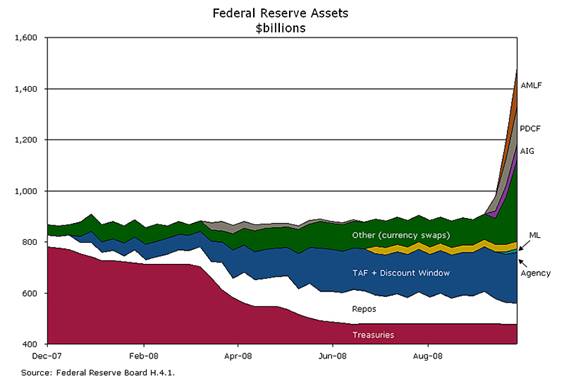

I have said a few weeks ago

Ben, You Have A Problem......".... The problem has not gotten smaller......Get ready for QE 2.0.........

Version 1.0 worked wonders for at least two weeks.....No wonder

Gold has a chance for a breakout ( via Zero Hedge ). I highly recommend to read the

entire piece and visit Mark Hanson & his Field Check Group site on a regular basis. Excellent stuff!

Vor einigen Wochen habe ich bereits getitels Ben, You Have A Problem....... Sieht so aus als wenn aus dem großen ein wirklich großes Problem geworden ist.....Wenn man weiß wie beschränkt Bernanke in seinem Denken ist gilt es als abgemachte Sache das wir uns auf eine massive Ausweitung des Quantitve Easing ( Notenpresse ) gefasst machen können. Macht ja auch Sinn wenn man sieht wie "toll" der erste Versuch funktioniert hat...... Da verwundert es wenig das Gold kurz davor ist "auszubrechen" ( via Zero Hedge ). Empfehle den kompletten Report zu lesen und den regelmäßigen Besuch von Mark Hanson und seiner Field Check Group Seite. Hier gibt es ungelfilterte "Bodenberichte" von der Hypotheken und Immobilienfront.

bigger / größer Thanks to

Karl Denninger5-28 - Potential Consequences of 5.5% Mortgage Rates Mr. Mortgage / Field Check Group

Mortgage Rates - It Could be as Bad as You Can Imagine

With respect to yesterday’s in the mortgage market — yes, it is as bad as you can imagine. No call can be made on the near-term, however, until we see where this settles out over the next week of so. If rates do stay in the mid 5%’s, the mortgage and housing market will encounter a sizable stumble. The following is not speculation. This is what happens when rates surge up in a short period of time - I lived this nightmare many times.

Yesterday, the mortgage market was so volatile that banks and mortgage bankers across the nation issued multiple midday price changes for the worse, leading many to ultimately shut down the ability to lock loans around 1pm PST. This is not uncommon over the past five months, but not that common either. Lenders that maintained the ability to lock loans had rates UP as much as 75bps in a single day.

Jumbo GSE money — $417k - $729,750 — has been blown out completely with some lender’s at 8%.

I have seen it all in the mortgage world — well, I thought I had.

A good friend in the center of all of the mortgage capital markets turmoil said to me yesterday “feels like they [the Fed] have lost the battle…pretty obvious from the start but kind of scary to live through it … today felt like LTCM with respect to liquidity.”

The consequences of 5.5% rates are enormous. Because of capacity issues and the long time line to actually fund a loan in this market, very few borrowers ever got the 4.25% to 4.75% perceived to be the prevailing rate range for everyone.

A significant percentage of loan applications (refis particularly) in the pipeline are submitted to the lenders without a rate lock.

This is because consumers are incented by much better pricing to lock for a short period of time…12-30 day rate locks carry the best rates by a long shot. But to get this short-term rate lock, the loan has to be complete enough to draw loan documents, which has been taking 45-75 days over the past several months depending upon the lender’s time line.

Therefore, millions of refi applications presently in the pipeline, on which lenders already spent a considerably amount of time and money processing, will never fund.

Furthermore, many of these ‘applicants’ with loans in process were awaiting the magical 4.5% rate before they lock — a large percentage of these suddenly died yesterday. From the lows of a month ago to today, rates are up 20%.

To make matters worse, after 90-days much of the paperwork (much taken at the date of application) within the file becomes stale-dated and has to be re-done with new dates — if rates don’t come down quickly many will have to be canceled out of the lender’s system.

To add insult to near-mortal injury, unless this spike in rates corrects quickly, a large percentage of unlocked purchases and refis will have to be denied because at the higher interest rate level, borrowers do not qualify any longer. For the final groin kicker, a 5.5% rate just does not benefit nearly as many people as a 4.5%-5% rate does. Millions already have 5.25% to 5.75% fixed rates left over from 2002-2006. .....

With respect to banks, mortgage banks, servicers etc, under-hedging a potential sell-off with the Fed supposedly having everybody’s back was a common theme. Banks could lose their entire Q2 mortgage banking earnings and middle market mortgage banker may never recover or immediately have to close shop

Lastly, consider sentiment — this is a real killer. This massive rate spike may have invalidated hundreds of billions spent to control the mortgage market literally overnight.

This leaves the mortgage and housing market very vulnerable.

Mortgage loan officers around the country are having a very very bad day today explaining to their clients why their rate was not locked and how rates are going to come right back down. They are also taking calls from borrowers with locked loans to confirm that the loan is indeed locked, inquiring as to when it will be approved or fund, and to rush the process in order to fund the loan by end of the lock-in term. This creates a customer service log-jam that chews through lender capacity quickly making the loan process even longer. Loans with second mortgages that need to be subordinated, are in a world of their own. Essentially, everything becomes a rush. Subsequently, loan officers will not feel like getting too aggressive taking new loan applications at least for the next month unless this corrects quickly.

Press surrounding this event will be the talk of Main Street immediately and cast a serious doubt over the housing recovery story that has been the common theme for months. An overnight housing market sentiment killer wildcard is something that nobody was factoring in.

We have to see where all this settles over the next few days before making a near to mid-term call on the outright damage because at this point, Fed or Treasury shock and awe is almost certain — another common theme has been ‘if it doesn’t work throw much more money at it’.

Obviously they have been following this closely for the past few weeks, as conditions began to deteriorate, and have likely been waiting to see where the upper range was before shocking in order to get maximum benefit…that would be a humongous short squeeze in Bonds driving rates lower. The problem is…if they do shock her and it is sold into with the same fury that we have been seeing, there may not be an act two.

The bond and mortgage market got complacent with the ultimate in moral hazard’s — the Fed’s got my back. Complacency is a killer.

Where we stand in two weeks in unknowable......

Labels: bernanke, housing, more "green shoots"....., mortgage market, qe

An "AAA" rating.....

An "AAA" rating.....

The following graph via

The following graph via

![[comparison2.jpg]](https://blogger.googleusercontent.com/img/b/R29vZ2xl/AVvXsEhp2lZ1pU_Ixt5OYPBM6izyW3NIlhQqWVI9gvzOR_jUUOsx-ySlaD7-BzXB39g20tI2yUxSDwzlVfbcc2yh05m5C6aAWz_SwXUpQVZk6p6u-nijXENKFsjmbHN9_-2AR46OEIWU/s1600/comparison2.jpg)

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/charts/metals/gold/t24_au_en_usoz_2.gif)

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/charts/metals/gold/t24_au_en_euoz_2.gif)

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}