What's a C.D.O.?

Ich kann mich nur FT Alphaville anschließen. Man sollte diesen Link all denen schicken die Besitzer dieser Papiere sind damit Sie endlich begreifen was für eine halsbrecherische Konstruktion den Weg in die Bücher gefunden haben und warum es täglich vorkommen kann das aus AAA über Nacht Junk werden kann. Ich denke da ganz besonders an ein paar deutsche Landesbänker......

Far and away one of the best graphics we’ve seen. Kudos to Felix Salmon and the people at Portfolio

Make sure you click here to start the interactive beauty!

Laßt euch dieses Schmuckstück nicht entgehen und klickt hier um die interaktive Schönheit zu betrachten.

It remains to be seen if the write down from Royal Bank Of Scotland is enough.... Maybe the age of the CDO portfolio is an explanation why they still value the mezzanine tranche with 70 percent..... The same CDO in 07 would be definitley close to zero....

Bin gespannt ob die Abschreibung der Royal Bank Of Scotland genug sein wird.....Evtl. ist ads bereits fortgeschrittenen Alter des CDO Portfolios ja die Erklärung dafür das die Mezzanine Tranche immer noch mit 70% bewertet wird. Ein CDO mit Baujahr 2007 würde wohl eher bei null notieren......

At 30 November, GBM's exposure to these super senior tranches, net of hedges and write-downs, totalled £1.1 billion to high grade CDOs which include commercial loan collateral as well as prime and sub-prime mortgage collateral, and £1.3billion to mezzanine CDOs based predominantly on residential mortgage collateral. The CDOs are largely based on ABS issued between 2004 and the firsthalf of 2006

And with news like this Surge in Auto-Loan DelinquenciesIs Latest Trouble for the Economy via the WSJ it should be clear that the problem is spreading to all parts of securitisations.

And with news like this Surge in Auto-Loan DelinquenciesIs Latest Trouble for the Economy via the WSJ it should be clear that the problem is spreading to all parts of securitisations.

Und mit Meldungen wie diesen Surge in Auto-Loan DelinquenciesIs Latest Trouble for the Economy dürfte auch bald der nächste Pfeiler der Verbriefungskredite mehr als nur leichte Schlgseite bekommen....

First came housing loans and the subprime-mortgage crisis.

Now, signs of stress are creeping into another key consumer area: auto loans.

Delinquencies in the auto-loan market are ticking up to their highest level in several years. Lenders are tightening terms in some cases, and interest rates have risen from the rock-bottom levels of a few years ago. About $575 billion in loans for new and used cars are made annually, according to the National Automotive Finance Association.

About 4.5% of auto loans made in 2006 to top-rated borrowers were at least 30 days delinquent as of the end of September, up from 2.9% the previous month,according to a Lehman Brothers survey of companies servicing these loans. That is the biggest one-month jump in at least eight years. Lehman says 12% of subprime borrowers, who have poorer credit records, were delinquent on their 2006 auto loans as of September. That is the highest level since 2002 and up from 11.1% the previous month.

![]()

Labels: "contained", "smart money", auto subprime, cdo, financial alchemy, harley davidson, level 3 accounting / mark-to-mark-believe gains, rating agencies, RBS

posted by jmf at 12:18 AM

6 comments

![]()

![]()

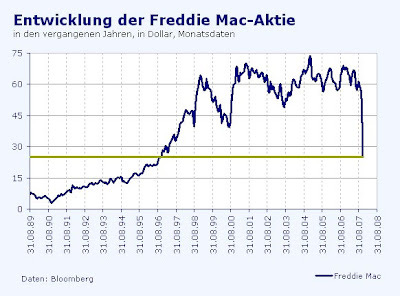

Freddie Mac, the second-largest U.S. mortgage company, warned of a possible cut in the dividend and the need for additional capital. The worst housing slump in 16 years caused ``significant deterioration'' in the third quarter that will continue through year-end, Freddie Mac said after reporting a net loss of $2.02 billion, or $3.29 a share, three times what some analysts estimated.

Freddie Mac, the second-largest U.S. mortgage company, warned of a possible cut in the dividend and the need for additional capital. The worst housing slump in 16 years caused ``significant deterioration'' in the third quarter that will continue through year-end, Freddie Mac said after reporting a net loss of $2.02 billion, or $3.29 a share, three times what some analysts estimated.

Citigroup, the biggest U.S. bank, will make $14.4 billion available immediately and as much as $7 billion more if GMAC meets certain conditions, GMAC said in a regulatory filing yesterday. The agreement replaces a $10 billion asset-backed funding facility that Citigroup provided GMAC in August 2006. Detroit-based GMAC didn't disclose the terms of the financing.....

Citigroup, the biggest U.S. bank, will make $14.4 billion available immediately and as much as $7 billion more if GMAC meets certain conditions, GMAC said in a regulatory filing yesterday. The agreement replaces a $10 billion asset-backed funding facility that Citigroup provided GMAC in August 2006. Detroit-based GMAC didn't disclose the terms of the financing..... Citigroup Ties

Citigroup Ties

Thanks to

Thanks to  The second worry, about the mortgage collateral, is particularly stark. Rating agencies badly misjudged default rates in subprime mortgages and are now having to downgrade reams of securities linked to them. With the credibility of ratings in tatters (there have even been calls for Warren Buffett to take over Moody's), investors have been left without a compass. For the time being, many would rather pull back than trust in their own analysis of credit risk. They are staying on the sidelines because they can't work out what securities are worth, not because they don't have the money to buy them.

The second worry, about the mortgage collateral, is particularly stark. Rating agencies badly misjudged default rates in subprime mortgages and are now having to downgrade reams of securities linked to them. With the credibility of ratings in tatters (there have even been calls for Warren Buffett to take over Moody's), investors have been left without a compass. For the time being, many would rather pull back than trust in their own analysis of credit risk. They are staying on the sidelines because they can't work out what securities are worth, not because they don't have the money to buy them.

thanks to

thanks to

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/charts/metals/gold/t24_au_en_usoz_2.gif)

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/charts/metals/gold/t24_au_en_euoz_2.gif)

{kind=link}