good take from pimco. please make sure you read the comments on the ofheo data that is used from pimco for their charts.

gute bestandsaufnahme von pimco. möchste euch noch besonders aie erläuterungen zu den ofheo daten hinweisen die ich eingefügt habe und die pimco in einigen bereichen (charts/text) zitiert.

In 2005, PIMCO forecasted home price appreciation (HPA) of 5% for 2006, with stronger gains in the first half of the year and smaller gains through the second half. The OFHEO (Office of Federal Housing Enterprise Oversight) home price index appreciated by 5.9% in 2006, with the largest gains occurring early in the year. This represented the smallest annual increase since 1999.

2006 marked an inflection point for the U.S. housing market. Although home prices continued to rise, the rate of increase slowed and some regions began to see price declines. The most drastic impact of the housing slowdown was felt in the subprime sector (mortgage loans to lower credit-quality borrowers) where mounting delinquencies and losses squeezed already-thin profit margins for mortgage lenders, forcing some to shut their doors. PIMCO believes that mortgage finance was critical to the rise in home prices since 2000, and also will be critical to the period ahead, which undoubtedly brings a correction of some sort. We want to answer the question: How much of a correction?

Housing Data

In 2005, PIMCO forecasted home price appreciation (HPA) of 5% for 2006, with stronger gains in the first half of the year and smaller gains through the second half. The OFHEO (Office of Federal Housing Enterprise Oversight) home price index appreciated by 5.9% in 2006, with the largest gains occurring early in the year. This represented the smallest annual increase since 1999. ( read more about the often misleading ofheo data

http://tinyurl.com/37mszm /

unter dem link mehr infos zu den nicht immer repräsentativen ofheo daten )this are comments from paul in jax and deb on the ofheo data.

- OFHEO data is great, but remember this news is about six months old

- The OFHEO data is not terribly relevant for many high priced metro areas.

The methodology uses only “TRANSACTIONS INVOLVING CONFORMING, CONVENTIONAL MORTGAGES PURCHASED OR SECURITIZED BY FANNIE MAE OR FREDDIE MAC”. - How many transaction in Los Angeles or similarly high priced cities meet this criteria? I would guess only a small fraction.

- So they are basing this entire index on the sales at the VERY BOTTOM entry level into the market, and most likely transactions involving somewhat more qualified buyers who can actually get standard financing meeting GSE guidelines.

Despite the continued growth of the average housing price, there was substantial variation between different regions. Several states saw price declines in the 4th quarter: California, Hawaii, North Dakota, Nevada, and Nebraska. Michigan became the first state to see a year-over-year decline in several years, primarily due to employment weakness in the auto industry.

thanks to barry ritholtz http://bigpicture.typepad.com/

thanks to barry ritholtz http://bigpicture.typepad.com/

Most housing indicators turned lower in 2006. New and existing home sales both fell during the year. Sales of existing homes were down 7% for the year and 13% from their 2005 peak. The drop in new home sales was slightly more pronounced, plummeting by as much as 23% before recovering to finish the year 11% lower. The number of vacant homes for sale increased by over 34% and homebuilders are coming under increasing pressure to control the surging inventories. The housing supply has continued to increase early in 2007 and the number of vacant homes for sale now stands at over 2.1 million (2.7% of all homes).

New vs. Existing Home Sales

The new home sales and price data for 2006 was volatile and we believe the reason is important. In the early ’90s California housing recession, only one of the top 10 builders was a public company. Today, nine of the top 10 homebuilders are public companies. This is important because equity investors punish public companies for high inventory. We have long expected to see the builders cut prices to unload new homes, which they did in 2006. We also believe prices were softer than the reported data reflect because instead of cutting the sales price, a builder often will include several thousand dollars of upgrades, which aren’t reflected in the sales-price data.

Existing home sales are a more stable indicator of sales volume for the bulk of the housing stock. Unlike new homes, where the owner is a builder who is a highly motivated seller, an existing homeowner will most often stay in the home rather than discount the price heavily. As a result, many existing homes that don’t sell quickly simply are taken off the market.

What’s More Important: Volumes or Prices?

We believe the volume of homes sold holds more significance because it has considerable second-order effects on the economy. A slowdown in housing leads to a reduction in employment not only for builders and construction-related sectors, but also for mortgage lenders, appraisers, brokers, and realtors. More importantly, it triggers a substantial decline in consumption. Fewer homes being sold means that there are fewer people buying new furniture, electronics, and other goods and services that normally accompany a new home purchase.

Mortgage Lending: Subprime Finally Weakens

If mortgage lending was fuel for the housing bonfire since 2000, it was the firehose in late 2006 and early 2007. ......

There is no doubt that higher HPA in previous years has limited losses from riskier loans, but performance for the 2006 vintage deteriorated rapidly amidst the combination of a housing slowdown and increasingly liberal underwriting standards

There is no doubt that higher HPA in previous years has limited losses from riskier loans, but performance for the 2006 vintage deteriorated rapidly amidst the combination of a housing slowdown and increasingly liberal underwriting standards

make sure you read this brilliant piece from rodger rafter with even scarier charts than the above from pimco. http://tinyurl.com/2fqgva

ihr solltet euch unbedingt noch mehr charts von rodger rafter ansehen. bitte auf den link klicken http://tinyurl.com/2fqgva

Tale of Two Mortgage Markets: Prime vs. Subprime

The rapid growth of subprime lending since 2000 and the innovation it has brought to the mortgage market generate a lot of interesting and alarming headlines, but the prime market actually comprises the majority of US mortgage loans, and has been unaffected substantially by the housing slowdown.

What distinguishes a prime loan from a subprime loan? Ask 10 mortgage professionals and you’re likely to get 10 slightly different answers, as there isn’t a single standard definition. ....

but it in very important to know that the last years subprime and alt-a have exploded! that is the area where the danger is......so the overall number from pimco gives only one side of the story. the foreclosures are coming in the segment fast and furious.....

but it in very important to know that the last years subprime and alt-a have exploded! that is the area where the danger is......so the overall number from pimco gives only one side of the story. the foreclosures are coming in the segment fast and furious.....

es ist allerdings sehr wichtig zu wissen, das der subprime und alt-a bereich in den letzen jahren explodiert sind. hier liegen die probleme. so die gesamtnummer gibt ein verzerrtes bild wieder. die zwangsvollstreckungen kommen genau aus diesem segment.

The prime market, on the other hand, is the traditional market that has served several generations of homeowners – typified by a 30-year or 15-year fixed rate, a 20% down payment, and a FICO or credit score above 700. The majority of these high-quality loans are sold into MBS (mortgage-backed securities) and guaranteed by one of the mortgage agencies – Ginnie Mae, Fannie Mae, or Freddie Mac. (Most subprime loans are not credit-eligible to be sold to the agencies.) Agency MBS have been unaffected by the housing slowdown.

Spreads on high quality MBS and AAA-rated ABS remain near historic tight levels, but lower-rated bonds have widened substantially. Investors increasingly are differentiating or tiering between originator/servicer quality, loan quality and many other aspects of mortgage credit – something PIMCO has been doing actively for some time. Mortgage credit analysis is granular, credit-intensive, and bond-specific. Generalities rarely apply.

The lenders that are most likely to emerge from the downturn are those with a significant, complementary prime mortgage business such as Countrywide, Wells Fargo, Chase, and Bank of America.

Outlook for 2007:

PIMCO expects the housing slowdown to continue in 2007 with a steeper decline in home sales than for home prices. New home prices should fall the most since they appreciated the most relative to existing housing during the run-up in prices. Attempts by homebuilders to reduce heavy inventories also will put downward pressure on new-home prices. The National Association of Realtors index, which tracks median home prices, should fall by 4-5% in 2007. The OFHEO index tracks repeat sales and PIMCO expects it to decline by over 1% this year (new home sales have little impact on this index).

The slowdown in housing should drag GDP down by approximately 1% over the next several quarters. Due to the multiplier effect that a slowdown has on consumption, it is likely that the impact on the economy will be even more substantial.

We expect the problems in the subprime market will result in continued consolidation of lenders, as the weaker players are not able to sustain loan production volumes or meet the tighter standards that are currently underway. Due to this consolidation, we expect to see subprime issuance decrease dramatically in 2007–2008. Much contraction has already taken place as year-to-date issuance has dropped nearly 10% compared to 2006 at this point in time. We envision a credit squeeze among low FICO, high loan-to-value and first-time homebuyers who are used to liberal credit standards.

It is likely that the poor performance we have seen in subprime loans will carry over to some degree into the most aggressively underwritten loans in the “Alt A” and possibly Jumbo prime markets.

We do not believe prime loans will be materially affected. The pronounced problems in the subprime market will not disappear as quickly as they emerged; instead we believe it will be a long process that will take perhaps years to correct.

PIMCO has often compared the housing market to a supertanker – a massive ship which takes 23 miles to come to a stop after being thrown into full reverse. (couldn´t resist..)

We believe we are in the middle of a downturn, not at the end, and that the problems created by expensive housing, overstretched consumer finance, and years of Fed tightening have yet to take their full toll on the US housing market.

Labels: alt-a, delinquencies, heatmap, ofheo, outlook 2007, pimco, prime, subprime

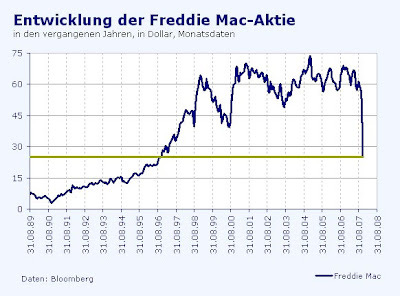

Freddie, Fannie Shares Will Continue to Slide, Jim Rogers Says

Freddie, Fannie Shares Will Continue to Slide, Jim Rogers Says  Freddie Mac, the second-largest U.S. mortgage company, warned of a possible cut in the dividend and the need for additional capital. The worst housing slump in 16 years caused ``significant deterioration'' in the third quarter that will continue through year-end, Freddie Mac said after reporting a net loss of $2.02 billion, or $3.29 a share, three times what some analysts estimated.

Freddie Mac, the second-largest U.S. mortgage company, warned of a possible cut in the dividend and the need for additional capital. The worst housing slump in 16 years caused ``significant deterioration'' in the third quarter that will continue through year-end, Freddie Mac said after reporting a net loss of $2.02 billion, or $3.29 a share, three times what some analysts estimated.

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/charts/metals/gold/t24_au_en_usoz_2.gif)

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/charts/metals/gold/t24_au_en_euoz_2.gif)