It will be interesting to see if the

fire sale to Abu Dhabi will be enough. With all capital ratios plunging and downgrades coming fast and furious i have some serious doubts.... But as long they can pay their dividend and they remain their creativity as shown in

No Kidding.... More Off Balance Sheet Vehicles For Citigroup everything is fine....Lets hope for them that this kind of deal won´t backfire like the famous

"Liquidity Puts" .... I highly recommend to see this video with the analyst

Meredith Whitney and hear her latest thoughts on Citigroup!

Es wird interessant zu sehen sein ob die Notoperation mit Hilfe von Abu Dhabi ausreichen wird. Da momentan alle Kapitalparameter im freien Fall sind und die Downgrades praktisch täglich eintreffen habe ich da so meine leichten Zweifel....Immerhin wollen sie weiter fleißig eine Dividende ausschütten und sind kreativ wie gewohnt wenn es darum geht die Bilanzen zu frisieren ( sieheNo Kidding.... More Off Balance Sheet Vehicles For Citigroup ) . Bleibt zu hoffen das diese Art an Konstruktion nicht wie die "Liquidity Puts" übelst zurückschlägt...... Zudem empfehle ich dringend sich das Video von der Analystin Meredith Whitney die vor einer Woche die große Krise bei Citi ausgelöst hat anzusehen. Es gibt doch noch Hoffnung das nicht alle Analysten vollkommen verblöded sind.

Dec. 1 (

Bloomberg) -- Moody's Investors Service may cut the top ratings on six of Citigroup Inc.'s seven structured investment vehicles as part of a review of $130 billion in SIV debt.

The net asset value of the $64.9 billion in Citigroup SIVs dropped to below or near 60 percent, prompting the ratings action, Moody's said in a statement yesterday. The junior notes of three of the funds have been downgraded to below investment grade.

> What a difference afew weeks made....Compare this action with the

Fact Sheet Citi-Advised Structured Investment Vehicles (SIVs) from mid October

> Was für ein Unterschied doch ein paar Wochen ausmachen.....Vergleicht das mit den Aussagen von Mitte Oktober Fact Sheet Citi-Advised Structured Investment Vehicles (SIVs) - The assets are of very high quality.

- The SIVs have no direct exposure to U.S. sub-prime assets.

- The SIVs have approximately $70 million of indirect exposure to sub-prime assets through securities such as collateralized debt obligations. Those securities are AAA-rated and carry credit enhancements.

- All assets are rated "A" or above; 80% - 90% are rated "AA" or

above; approximately 50% are rated "AAA"

SIVs, which sell short-term debt to buy longer-term, higher-yielding assets, were shut out of the short-term market as losses on subprime mortgage securities prompted investors to retreat from all but the safest of securities. Unable to finance themselves, three SIVs have defaulted and others are being bailed out by their sponsors. The world's 30 SIVs have more than $300 billion of assets.

SIVs, which sell short-term debt to buy longer-term, higher-yielding assets, were shut out of the short-term market as losses on subprime mortgage securities prompted investors to retreat from all but the safest of securities. Unable to finance themselves, three SIVs have defaulted and others are being bailed out by their sponsors. The world's 30 SIVs have more than $300 billion of assets.

``In recent weeks, Moody's has observed material declines in market value across most asset classes in SIV portfolios,'' the ratings company said in the statement.

Moody's said it surveyed 20 SIVs since Nov. 7 and expanded its review after noticing ``significant additional deterioration'' in asset values.

Moody's cut $14 billion in debt in all, mostly capital notes that rank below commercial paper and medium-term notes and are usually the first to absorb losses, Henry Tabe, managing director in charge of structured finance, said in a telephone interview. The ratings company placed $105 billion of debt on review for a downgrade and confirmed the ratings on $11 billion, Tabe said.

Links Finance Corp., a SIV sponsored by Bank of Montreal with $19.1 billion of debt, also had its junior notes cut and may have the remainder downgraded, Moody's said.

`Continued Deterioration'

SIV assets on average are 38 percent financial institution debt, 16 percent asset-backed securities and 12 percent collateralized debt obligations, Moody's said.

The downgrades are ``a reflection of the continued deterioration in market value of SIV portfolios combined with the sector's inability to refinance maturing liabilities,'' Moody's said. Net asset values have slumped to 55 percent from 102 percent in June, Moody's said, including the NAVs of the three defaulted SIVs.

Citigroup, the largest U.S. bank by assets, provided $7.6 billion of emergency financing to the seven SIVs it runs earlier this month after they were unable to repay maturing debt.

Citigroup, based in New York, created the first SIV in 1988 and is the largest manager.

The SIVs' struggle for survival, and the threat of having their assets dumped on the market, prompted Treasury Secretary Henry Paulson to broker talks with Citigroup, JPMorgan Chase & Co. and Bank of America Corp. to form an $80 billion

"Superfund" to help bail them out.

Centauri, Beta

HSBC this week said it will take on $45 billion of assets from the two SIVs it manages after they were unable to finance themselves. SIVs set up by Dusseldorf- based lender

IKB and London-based

Cheyne Capital Management Ltd. defaulted last month after investors stopped buying their asset-backed commercial paper.

Citigroup said in a Nov. 5 regulatory filing that it ``will not take actions that will require the company to consolidate the SIVs.'' The strategy ``remains unchanged from the disclosures in the third quarter'' filing, spokesman Jon Diat said yesterday in an e-mail statement. ``We continue to focus on liquidity and reducing leverage,'' Diat said. Citigroup's SIV assets have dropped to $66 billion from $83 billion on Sept. 30, Diat said.

Centauri Corp., the largest SIV run by Citigroup with $16.9 billion of debt, had its P1 commercial paper rating placed on review for downgrade as well as its AAA medium-term note program, Moody's said. Centauri's net asset value dropped to 60 percent from 85 percent since Sept. 5, Moody's said.

Beta Finance Corp., the second-largest Citigroup SIV with $16 billion of debt, had its senior debt ratings placed on review for downgrade after its net asset value declined to 60 percent from 87 percent, Moody's said.

Sedna, Dorada

Four other Citigroup SIVs, Sedna Finance Corp., with $10.7 billion of debt, Five Finance Corp., with $10.3 billion, Dorada Corp. with $8.5 billion, and Zela Finance Corp., with $2.5 billion, had their P1 commercial paper rating and AAA medium- term note programs placed on review, Moody's said.

Sedna's net asset value dropped to 56 percent, Five's declined to 63 percent, Dorada dropped to 62 percent and Zela's fell to 61 percent. A seventh Citigroup SIV, Vetra Finance Corp., wasn't part of the review.

The capital notes of Dorada, Beta and Centauri were reduced 11 levels to Caa3 from Baa1.

Labels: "Master Liquidity Enhancement Conduit", baliout, citigroup, core capital, creative accounting, meredith whitney, off balance sheet, siv´s, tier 1 capital

FT

FT

I especially agree with the first quote.....

I especially agree with the first quote.....

Nov. 26 (

Nov. 26 ( Citigroup will sell equity units to the Abu Dhabi Investment Authority that convert into common shares, the New York-based lender said today in a press release.

Citigroup will sell equity units to the Abu Dhabi Investment Authority that convert into common shares, the New York-based lender said today in a press release. Charles O. Prince III (

Charles O. Prince III (  Nov. 26 (

Nov. 26 (

One company is follow closely is

One company is follow closely is

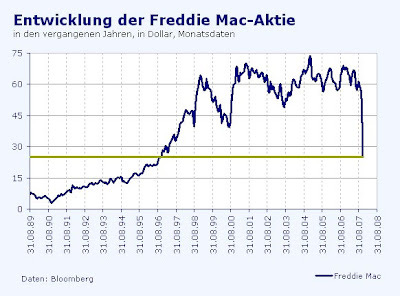

Freddie Mac, the second-largest U.S. mortgage company, warned of a possible cut in the dividend and the need for additional capital. The worst housing slump in 16 years caused ``significant deterioration'' in the third quarter that will continue through year-end, Freddie Mac said after reporting a net loss of $2.02 billion, or $3.29 a share, three times what some analysts estimated.

Freddie Mac, the second-largest U.S. mortgage company, warned of a possible cut in the dividend and the need for additional capital. The worst housing slump in 16 years caused ``significant deterioration'' in the third quarter that will continue through year-end, Freddie Mac said after reporting a net loss of $2.02 billion, or $3.29 a share, three times what some analysts estimated.

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/charts/metals/gold/t24_au_en_usoz_2.gif)

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/charts/metals/gold/t24_au_en_euoz_2.gif)

{kind=link}