hallo,

das ist zwar etwas länger aber mit das beste was ich bisher an wandlung eines bullen in einen bären innerhalb von jna. bis kuly dieses jahr zu lesen bekommen habe. kann das wirklich nur jedem empfehlen. ist wirklich beeindruckend und paßt hervorragen dzu den gerade veröffentlichten gdp zahlen. habe das im übrigen von einem der besten blogs im web

http://globaleconomicanalysis.blogspot.com/ (s. auch linkleiste)

Lights Out in GeorgiaFollowing is a set of posts from a real estate broker who goes by the name "Sonnypage" on the Motley Fool. This synopsis is with his permission. Follow the progression

from 2006-01-04 through 2006-07-20 (4.12006-20.7.2006). You might find it interesting.

2006-01-04Many of you know by now that my wife and I are both Realtors and associate brokers. We live and work north of Atlanta in the suburbs of Alpharetta and Roswell. I made the point in a post last month that I have always thought that our business gives us some unique insights into the economy, not just here in Atlanta, but across the country.

We are seeing an extremely high level of relocation activity. Our business last year was very solid, we closed twenty six transactions. So far this year, days into the year, we have two transactions pending, booked in the fourth quarter, plus twenty five prospects. If only two thirds of those prospects close, then we already have eighteen or so deals. They are evenly split, buyers and sellers, but much more importantly, nineteen involve relocations. This is a very high level of relocation activity, the highest we have seen in years.

More relocation prospects than any January in memory.

The economy remains very strong.

Mish and I would seem to have very different points of view on what 2006 holds in store. I am basing my forecast on what I am seeing, and what I am seeing is a strong economy.

There will be no recession in 2006.Sonnypage

2006-01-30Last week my wife and I met our out of town buyers at the home that we had put under contract earlier in the month. It was time to meet a home inspector at the home for the inspection. The inspection took most of the day, so we had plenty of time to talk about anything and everything.

The mortgage lender and I were both amused by all the chatter in the popular press about the "real estate bubble". He told me that his business is up about 20% over last January. I told him that we were having the strongest January we have ever had. It is truly remarkable. About then his sister, the buyer wife, walked into the room where we were talking. I asked them both, what would this home be worth back in northern Virginia? We were under contract here in Alpharetta at $1.1 million. The buyer wife paused for just a second, then said she thought about $2 million. Her brother, the mortgage lender, thought a second longer, then said he thought perhaps closer to $2.5 million.

Where's your housing recession, Mish? In actuality, if our economy is growing, the nations' total wealth is growing, then real estate as a whole, nationwide, continues to appreciate.

Our business here on Atlanta's north side is very strong. We have four contracts year to date, we will get number five this week. This compares with twenty six closings in 2005, so we are clearly off to a strong start. The unemployment rate here is 3.2 %, below the national average. Business is booming. I know of no one complaining of slow business, or worried about losing their job. Everyone is too busy making money to have time to worry. As for us and our business, our average transaction continues to move up in dollar size. If 2000 was our biggest year with forty four transactions, we could easily make more dollars this year with as few as perhaps thirty deals.

We are seeing lots of money out there, it's full speed ahead. A very bright year lies ahead.

All of which leaves me free to make my biggest and strongest Sonnypage prediction ever. This time next year, I will still be making money hand over fist, and Mish and Gary Shilling and the rest of the doomsday crowd will still be pumping the next depression. And as always, it will still be just over the horizon, not quite here yet, but surely coming, right?

Sonnypage

2006-04-07If I am reading Mish correctly, he still is calling for a sharp pullback in residential housing in the U.S. that will lead us into a recession. Mish, if I am misstating you please correct me, and I am still taking the other side of your bet. It's not going to happen.

Real estate is local.

I have no doubt that Florida, southern California and other hot spots are having contractions. The speculative money has bailed out and that's what happens. But here in Atlanta, where my wife and I have our residential real estate business, it's a very different story. We never had a speculative run up in prices here and so far, this year, it's shaping up as a normal year. We have nine transactions closed or pending year to date, which is exactly where we were this time last year. We currently have six listings, two of which are pending, and those pending listings, plus two others that have already closed, are going at about 97% of list price. Obviously, that does not translate as a distressed market. We have the same situation on the buy side. Our buyers under contract are paying about 97% of list. We have not been able to find distressed sellers for our buyers in upscale neighborhoods willing to sell at major discounts to list price. The only other part of the country that I can offer direct evidence of is Houston. My brother in law is a builder while my sister and one of her daughters are a mother-daughter realtor team. Here is an email from my sister from last week about the Houston real estate market.

We put a $ 1.5 mil house under contract today and met with someone yesterday about our $2.7 mil spec. (*Daughter*) showed a house to a couple her age that was priced at $469,000- a 3/2 one story bungalow in West U. They were one of five competing bids and did not get it with their offer of $475,000. It was not under priced. We are having the best market we have ever had city wide.

A collapsing real estate market, Mish? I don't think so.Sonnypage

2006-04-30Most of you know by now that my “day job” is real estate. My wife and I practice real estate north of Atlanta up in Roswell and Alpharetta. As Mish continues to pound away trying to make the point that residential real estate is doomed or worse, I feel honor bound to jump in every now and then and

remind everyone that real estate is local, local, local. That means that even if real estate is in trouble in say, Florida, it's still, according to my sister, doing extremely well in Houston, and very well, I would say, in Atlanta. We have twelve deals closed or pending through

April which is about where we were this time last year. It's looking like a twenty five deal year which is fine.

Sonnypage

2006-06-10This year is quickly becoming what might euphemistically be called a character building experience.

We are off to the slowest start in the twelve years we have been in business. Here's a taste of what we are up against. Two months ago we took a great listing in Alpharetta just to the north of us. It's a beautiful three sides brick, full finished basement, in a cul de sac. They listed at $550,000, which was actually a little below what we recommended. They are definitely motivated to sell. When we had lots of looks but no offers, they agreed to drop the price to $535,000. I emailed all agents who had previously shown the house to advise of the price drop, and sure enough, one agent brought his buyers back for a second, then third, look. They offered $495,000. We countered at $530,000. Our sellers said they really did not want to go that much lower. I was not too concerned. I expected a counter from the buyers, then another counter from my sellers and we would eventually get there. The next morning, when I did not hear back from the buyer's agent, I gave him a call. Did I get a shock, they were done, that was it, no higher offer. So what we have are buyers who just don't want to pay too much, who are really skittish, and sellers who are having trouble accepting that things are slowing down. Two years ago, or even last summer, we would have that house under contract. But not this year. We now have a total of six listings, five of which have reduced, the other is brand new. Only one really active buyer, plus two of the listings who will buy locally if they can first sell.

If things don't pick up fairly quickly, this will be our slowest year ever. We have closed or have pending a total of only twelve transactions year to date. We have booked only one contract since May 1st which is really slow. Our business plan was thirty transactions, I would have been o.k. with twenty six, but at this rate we will not reach twenty. This is normally our peak season. If Atlanta, which has been a solid market with no speculative price run ups, is faltering, then

I suspect that this slow down has become national at last, no longer just local.

The economy is slowing and is doing so rather quickly. In my opinion, at least, the chances of a recession starting no later than the first quarter have increased significantly.

Sonnypage

2006-07-20Most of the regulars here know that my wife and I are a Realtor team associated with one of the major national firms here on Atlanta's north side, out in Roswell and Alpharetta. It's been a “character building year” as another agent in our office put it the other day. What makes it more stunning, at least to me, is that it started out so well.

We ended the first quarter with nine deals pending or closed, which is a very solid start. Then we hit a brick wall with only three deals in

the second quarter and that would make it our worst second quarter ever in our twelve years.Then it got worse. Normally, over the years, about one in fifteen deals fall out, that is, they fail to close. Usually it's over the inspection contingency amendment but not always. At any rate, two of our three second quarter contracts failed to close. Unbelievably we booked and closed only one contract in the second quarter. So here we are, July 20th, with only ten deals for the year. What a mess.

How those two contracts failed just might tell a story about this years' market and the economy in general. First, one of them was indeed over the inspection amendment. Most of you understand that after going under contract, the buyer is entitled to have a qualified home inspector do an inspection. The buyer then presents a copy of the inspection to the seller along with an amendment to the contract asking for the repair of defects affecting safety or the structural integrity of the home. In this instance, the buyer went far beyond that, asking for, at least in my opinion, cosmetic items and home improvements. Our sellers' response, I thought, was more than fair, but the buyer would not yield. Normally we can work these differences out but not this time. Looking back, it is clear that the buyer was determined to wring additional concessions out of the seller or not close. We had a failed agreement and both parties signed a termination and release as required. That listing is back on the market.

Then the other failed contract was even more unusual. We had been working with relocation buyers from Cincinnati for several months. We found them a great house and went under contract. Ten days before closing they called to say they had decided they did not want to move. [Instead] he is leaving the company [that was] trying to move him to Atlanta. My take on this is he was afraid they would move him down here and then let him go. His company is facing a management reshuffle. But, who knows? At any rate, it cost him $5500, his forfeited earnest money.

So here we are with ten deals and needing a total of about twenty to meet our cash flow needs; personal and business plus taxes. The last year we failed to “make a living” so to speak in real estate was about 1994. Without a strong finish we just may be looking at that again. What are our chances of pulling it out? It's still possible. We have several buyer prospects plus we have ten listings and listings are the life blood of any real estate business. We will, with certainty, get one more listing by month's end. On the other hand, we have a listing that expires at midnight Monday and we don't expect them to renew. They have had two lowball offers and have refused both. My take is that they can't reduce without going under water.

What do you do if you owe more on your home than you can sell it for? Apparently, you just decide to sit on it and hope for a better market, at least for now.

Sonnypage

Mish (from here on down):For one reason or other realtors across the country thought "It's different here"."We are unique". "Real estate is local". "It won't happen here". "There is no bubble".

Look at all the reasons given:-Demographics - Florida & California

-Strong Jobs - California

-Relocations - Atlanta and SE

-Retirement - Las Vegas, Phoenix, Florida

-Strong economy - Everywhere but the rust belts

-This place is unique - Damn near everywhere

And in every case my set of answers was the same.-Home prices have outstripped wages by 4-5 standard deviations from normal

-Home prices have outstripped rents by 4-5 standard deviations from normal

-This can't continue

-What can't continue won't continue by definition

One by one by one all of the local experts that said "It's different here" are finding out "It's NOT different here".

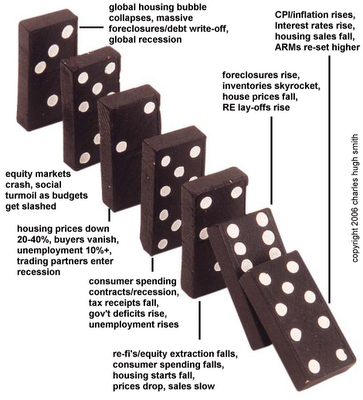

The "strong economy" was (and still remains) an illusion. What we had was an economy totally propped up by homebuilding and real estate transactions. 40% of all home buying in both 2004 and 2005 was for second homes or for "investments". In addition people were all too quick to spend that increased "wealth" from home price appreciation (and then some), going deeper and deeper in debt.

The economy has not crashed (yet) because homebuilders are still building. That supports jobs. But when those houses don't sell (and they won't - without enormous discounts) all this "paper wealth" of homeowners is going to vanish overnight. As soon as someone drops their price by $100,000 every house in the neighborhood will be repriced. Comps will drop like a rock. Consumers used to seeing nothing but rising prices are in for a rude awakening. Their house will no longer be an ATM. Consumer spending is 75% of the economy and it has only one way to go and that is down. There are going to be a lot of people hurt badly in the recession of 2007.

The Blame GameIt will be interesting to see who the scapegoats will be.

Some will blame Realtors

Some will blame the Fed for hiking rates too far

Some will blame the homebuilders for slashing prices

Some will blame their neighbors for selling too low

Where the blame really belongs.

On the Fed (not for raising rates) but for cutting them to 1% in the first place and flooding the world with dollars in the biggest liquidity experiment the world has ever seen

On banks and Fannie Mae for loose lending standards

On government for promoting the "ownership society"

On themselves for getting caught up in bubble madness just as they did with stocks in 2000, then taking cash out refis and spending like drunken fools further fueling a runaway economy

That was a friendly debate with Sonnypage on the FOOL, not an acrimonious one. I am pretty sure Sonnypage will harbor no ill will towards me for making this post, especially since I asked in advance if he minded. Sonnypage was gracious enough to say yes. I think he wants to share a "prepare for the worst" message with others that might think "It can't happen here", "The local economy is too strong".

A recession is just around the corner.Ironically enough, it has already started for Sonnypage.

Mike Shedlock / Mishhttp://globaleconomicanalysis.blogspot.com

wow! wenn das kein augenöffner ist was dann. das sagt wohl mehr als alle statistiken und die so "solide" und in "guter verfassung" befindliche us wirtschaft.gruß

jan-martin

das ist er.

das ist er.

1/153 This is looking toward the Gaslamp district and the construction site of The Hard Rock Condotels in the foreground. Several cranes and half empty or half finished condos in the background. The number of huge holes in the ground awaiting condos to be built on them is just silly, but harder to photograph. Many of these places also have HOA fees of $600-800 a month for a tiny living space.nd the construction site of The Hard Rock Condotels in the foreground. Several cranes and half empty or half finished condos in the background. The number of huge holes in the ground awaiting condos to be built on them is just silly, but harder to photograph.

1/153 This is looking toward the Gaslamp district and the construction site of The Hard Rock Condotels in the foreground. Several cranes and half empty or half finished condos in the background. The number of huge holes in the ground awaiting condos to be built on them is just silly, but harder to photograph. Many of these places also have HOA fees of $600-800 a month for a tiny living space.nd the construction site of The Hard Rock Condotels in the foreground. Several cranes and half empty or half finished condos in the background. The number of huge holes in the ground awaiting condos to be built on them is just silly, but harder to photograph.

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/charts/metals/gold/t24_au_en_usoz_2.gif)

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/charts/metals/gold/t24_au_en_euoz_2.gif)