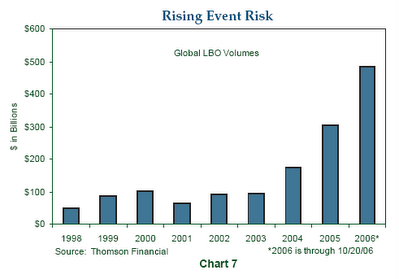

Only 35% Of Survey Participants Expect The Stess Test To Be Credible....

I´m surprised that the rate is above 20 percent... ;-)

Ich bin ehrlich überrascht das immerhin 35% dem Stresstest eine Aussagekraft zubilligen.... ;-)

Goldman Sachs via FT Alphaville

GS Stress Test

H/T Zero Hedge

Get ready for at least a weekend full of spin......

Man kann sich jetzt schon einmal mindestens auf ein Wochenende voller "Spin" einstellen.....

UPDATE:

I assume after the results the percentage of believers hasn´t increased "significantly"....

Kann mir gut vorstellen das nach Bekanntgabe der Ergebnisse die Glaubwürdigkeit des Tests nicht "explosionsartig" hinzugewonnen hat....

Stress Test Results CEBS

Apparently Not Too Stressful The Mess That Greenspan Made

Stress test’s sovereign support = senseless

Gaming the stress tests 101 FT Alphaville

Morgan Stanley On Stress Tests: "Lots Of Missed Opportunities" ZH

Van Steenis European Stress Tests

Ich bin ehrlich überrascht das immerhin 35% dem Stresstest eine Aussagekraft zubilligen.... ;-)

Goldman Sachs via FT Alphaville

It’s the results of a Goldman Sachs survey of 376 mostly-European market “participants” ahead of the results

GS Stress Test

H/T Zero Hedge

Get ready for at least a weekend full of spin......

Man kann sich jetzt schon einmal mindestens auf ein Wochenende voller "Spin" einstellen.....

UPDATE:

I assume after the results the percentage of believers hasn´t increased "significantly"....

Kann mir gut vorstellen das nach Bekanntgabe der Ergebnisse die Glaubwürdigkeit des Tests nicht "explosionsartig" hinzugewonnen hat....

Stress Test Results CEBS

5 Cajas ( Spain ), Ate Bank (Greece ), Hypo ( Germany ) failed....

CEBS SAYS 7 BANKS HAD OVERALL SHORTFALL OF EU3.5 BLN OF TIER 1Stress Test Interactive Graph Spiegel

Apparently Not Too Stressful The Mess That Greenspan Made

Stress test’s sovereign support = senseless

the test parameters being rather cynically calibrated to achieve the desired result.JPMorgan Shreds The Stress Tests, Says 54 Banks Should Have Failed, And That Investors Will Lose Confidence BI

Gaming the stress tests 101 FT Alphaville

Morgan Stanley On Stress Tests: "Lots Of Missed Opportunities" ZH

Van Steenis European Stress Tests

Labels: "Enron-esque characteristics", anti spin, balance sheet quality, moral hazard, regulatory failure, stresstest, tier 1 capital

posted by jmf at 6:08 AM

0 comments

![]()

![]()

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/charts/metals/gold/t24_au_en_usoz_2.gif)

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/charts/metals/gold/t24_au_en_euoz_2.gif)